Corpsec HotlineMay 16, 2011 Government Permits FDI in LLPs: A Welcome Move, But Restrictions May Be A DampenerIn a welcome move, the Cabinet Committee on Economic Affairs of the Government of India (“Committee”) has finally approved the proposal to allow foreign direct investment (“FDI”) in limited liability partnerships (“LLPs”). The proposal allows FDI in LLPs that operate in sectors where no monitoring is required. While such investments into an LLP structure require prior governmental approval, it still opens up an opportunity for FDI investors for structuring their Indian investments in a tax efficient manner1. LLPs are hybrid entities, formed and incorporated under the LLP Act, 2008, possessing characteristics of both companies and partnerships and are considered a good alternative to companies in many jurisdictions. It is expected that the Department of Industrial Policy and Promotion (“DIPP”) would roll out a notification in future to give effect to the Committee’s approval (“Approval”). Through this update, we intend to provide an insight into the intricacies of the Approval, the various conditions prescribed therein and some further expectations which remain to be fulfilled. Introduction Stakeholders had long been expecting the regulators to permit foreign investment into LLPs; ever since the LLP Act, 2008 was notified in January 2009. Such expectations soared but were left unfulfilled, at the time of issue of the Consolidated FDI Policy in April, 2011 (“FDI Policy”)2. The Approval in that sense, acknowledges a long standing demand of stakeholders; but with a lot of caveats. Importantly, the Approval specifically provides that LLPs would not be able to avail the benefits of the Foreign Institutional Investor, the Foreign Venture Capital Investor and the External Commercial Borrowing routes of raising foreign investments, for the time being. The conditions prescribed, by the Committee, on FDI in LLPs, can be categorized under the following broad heads viz (i) investment restrictions, (ii) funding restrictions, and (iii) ownership and management restrictions; each of which is discussed below in greater detail. Investment Restrictions FDI in LLPs has been approved subject to the following important conditions:

While the Approval does not provide for a clear definition of the expression ‘FDI linked performance related conditions’; this expression may be interpreted to refer to the investment conditions prescribed under the FDI Policy for certain sectors, which may be in the nature of minimum capitalization requirements, or a lock-in of investments etc. Consequently, LLPs may not appeal as a viable option in sectors such as real estate or non-banking financial business, which seek foreign investment, losing an edge to the traditional option i.e. companies. Further, unlike corporate structures, LLPs that have received FDI are disqualified from making any downstream investments. This restriction may make LLPs unviable for multiple tier holding structures in India. Funding Restrictions

Permitting downstream investments by companies into LLPs may provide some flexibility for foreign owned entities in terms of downstream investments. By way of an illustration, please refer to Figure 1 below for a possible structure of FDI (in Approved Sectors) in India. Fig 1: Investments in Approved Sectors Ownership and Management Restrictions

Analysis The Approval has been coupled with certain onerous restrictions due to which LLPs may lose a competing edge against corporate structures, for the time being. Further, restricting FDI to LLPs only in the Approved Sectors and prohibiting downline investments by such LLPs may prove to be an impediment on their use in structuring businesses in India, since one of the most important advantages of an LLP is that LLPs are not subject to dividend distribution tax, which benefit may not be available in absence of use of LLPs for multi-tier holding structures. Additionally, the Reserve Bank of India (“RBI”) may be required to issue separate notifications setting out the disclosure and filing requirements, including revising the current forms to provide for situations where LLPs receive FDI. The Approval is also silent on the point of entry and exit pricing and valuation, which is expected to be clarified by RBI shortly. Presently, these changes appear more to be in the nature of testing the waters by the government for permitting FDI in LLPs. Hopefully, as the Approval itself provides, ‘FDI in LLPs will be implemented in a calibrated manner’. As things progress, the Government may remove the shackles imposed on FDI in LLPs, with more experience building in using LLPs as structural alternatives. ____________________________ 1 Currently, LLPs are not subject to any dividend distribution tax which is currently leviable on companies at a rate of 15% (subject to applicable surcharge and education cess) 2 Refer to our Hotline dated April 5, 2011 on the Consolidated FDI Policy. 3 As per the LLP Act, 2008, a Designated Partner shall be the person responsible for and liable in respect of the compliances stipulated for an LLP.

You can direct your queries or comments to the authors DisclaimerThe contents of this hotline should not be construed as legal opinion. View detailed disclaimer. |

|

In a welcome move, the Cabinet Committee on Economic Affairs of the Government of India (“Committee”) has finally approved the proposal to allow foreign direct investment (“FDI”) in limited liability partnerships (“LLPs”). The proposal allows FDI in LLPs that operate in sectors where no monitoring is required. While such investments into an LLP structure require prior governmental approval, it still opens up an opportunity for FDI investors for structuring their Indian investments in a tax efficient manner1.

LLPs are hybrid entities, formed and incorporated under the LLP Act, 2008, possessing characteristics of both companies and partnerships and are considered a good alternative to companies in many jurisdictions. It is expected that the Department of Industrial Policy and Promotion (“DIPP”) would roll out a notification in future to give effect to the Committee’s approval (“Approval”). Through this update, we intend to provide an insight into the intricacies of the Approval, the various conditions prescribed therein and some further expectations which remain to be fulfilled.

Introduction

Stakeholders had long been expecting the regulators to permit foreign investment into LLPs; ever since the LLP Act, 2008 was notified in January 2009. Such expectations soared but were left unfulfilled, at the time of issue of the Consolidated FDI Policy in April, 2011 (“FDI Policy”)2. The Approval in that sense, acknowledges a long standing demand of stakeholders; but with a lot of caveats. Importantly, the Approval specifically provides that LLPs would not be able to avail the benefits of the Foreign Institutional Investor, the Foreign Venture Capital Investor and the External Commercial Borrowing routes of raising foreign investments, for the time being. The conditions prescribed, by the Committee, on FDI in LLPs, can be categorized under the following broad heads viz (i) investment restrictions, (ii) funding restrictions, and (iii) ownership and management restrictions; each of which is discussed below in greater detail.

Investment Restrictions

FDI in LLPs has been approved subject to the following important conditions:

- FDI in LLPs could only be with government approval, the approving authority being the Foreign Investment Promotion Board (“FIPB”).

- In line with the restrictions currently placed for partnership firms, the Approval specifically prohibits LLPs that have received FDI from engaging in agricultural or plantation activities, print media and real estate business.

- Further, for an LLP to become eligible to raise FDI, it should operate in such sectors or undertake such activities in which 100% FDI under automatic route is permissible, without any FDI linked performance related conditions (“Approved Sectors”).

While the Approval does not provide for a clear definition of the expression ‘FDI linked performance related conditions’; this expression may be interpreted to refer to the investment conditions prescribed under the FDI Policy for certain sectors, which may be in the nature of minimum capitalization requirements, or a lock-in of investments etc. Consequently, LLPs may not appeal as a viable option in sectors such as real estate or non-banking financial business, which seek foreign investment, losing an edge to the traditional option i.e. companies.

Further, unlike corporate structures, LLPs that have received FDI are disqualified from making any downstream investments. This restriction may make LLPs unviable for multiple tier holding structures in India.

Funding Restrictions

- The Approval provides that FDI in LLPs would be allowed only by way of cash received by inward remittance through normal banking channels or through debit to Non-resident External Rupee account or Foreign Currency Non-resident account of a person, maintained with an authorized dealer or an authorized bank.

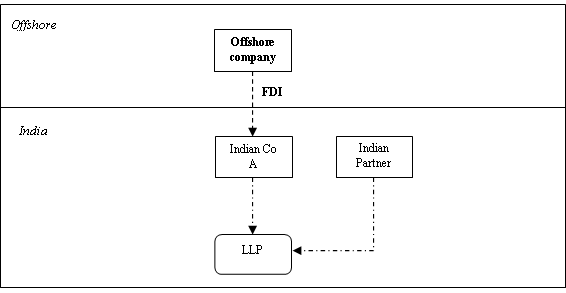

- An Indian company having FDI would be permitted to make downstream investment in an LLP provided both the investing company and the investee LLP operate in Approved Sectors.

Permitting downstream investments by companies into LLPs may provide some flexibility for foreign owned entities in terms of downstream investments. By way of an illustration, please refer to Figure 1 below for a possible structure of FDI (in Approved Sectors) in India.

Fig 1: Investments in Approved Sectors

Ownership and Management Restrictions

- As per the LLP Act, every LLP is required to have at least one designated partner (“Designated Partner”)3 who is ‘resident in India’. The Approval provides that the expression ‘resident of India’ with reference to a Designated Partner of an LLP desirous of raising FDI, would be ascertained as per the criteria laid down under sections 2(v)(1)(A) and 2(v)(1)(B) of the Foreign Exchange Management Act, 1999 (“FEMA”).

- The Approval provides that in case where an LLP has a body corporate as the Designated Partner, such body corporate should be a company registered under the Companies Act, 1956 and not any other LLP or trust etc.

- Finally, the Approval also provides that a company, which has FDI in it, shall not be permitted to convert to an LLP except without prior FIPB approval. Further, such companies would also be required to comply with the other conditions of the Approval, as prescribed for LLPs, in spirit.

Analysis

The Approval has been coupled with certain onerous restrictions due to which LLPs may lose a competing edge against corporate structures, for the time being. Further, restricting FDI to LLPs only in the Approved Sectors and prohibiting downline investments by such LLPs may prove to be an impediment on their use in structuring businesses in India, since one of the most important advantages of an LLP is that LLPs are not subject to dividend distribution tax, which benefit may not be available in absence of use of LLPs for multi-tier holding structures. Additionally, the Reserve Bank of India (“RBI”) may be required to issue separate notifications setting out the disclosure and filing requirements, including revising the current forms to provide for situations where LLPs receive FDI. The Approval is also silent on the point of entry and exit pricing and valuation, which is expected to be clarified by RBI shortly.

Presently, these changes appear more to be in the nature of testing the waters by the government for permitting FDI in LLPs. Hopefully, as the Approval itself provides, ‘FDI in LLPs will be implemented in a calibrated manner’. As things progress, the Government may remove the shackles imposed on FDI in LLPs, with more experience building in using LLPs as structural alternatives.

____________________________

1 Currently, LLPs are not subject to any dividend distribution tax which is currently leviable on companies at a rate of 15% (subject to applicable surcharge and education cess)

2 Refer to our Hotline dated April 5, 2011 on the Consolidated FDI Policy.

3 As per the LLP Act, 2008, a Designated Partner shall be the person responsible for and liable in respect of the compliances stipulated for an LLP.

You can direct your queries or comments to the authors

Disclaimer

The contents of this hotline should not be construed as legal opinion. View detailed disclaimer.

Research PapersLittler International Guide (India) 2024 Unmasking Deepfakes Are we ready for Designer Babies |

Research ArticlesThe Bitcoin Effect Acquirers Beware: Indian Merger Control Regime Revamped! Navigating the Boom: Rise of M&A in Healthcare |

AudioDigital Lending - Part 1 - What's New with NBFC P2Ps Renewable Roadmap: Budget 2024 and Beyond - Part I Renewable Roadmap: Budget 2024 and Beyond - Part II |

NDA ConnectConnect with us at events, |

NDA Hotline |